Guided reading

According to the calculation data given by various relevant research institutions, the planned production capacity of my country’s automotive power batteries is expected to reach 3TWh in 2025, which is 10 times that of 2021. Among them, the 2025 production capacity plans announced by CATL, BYD, China Innovation Aviation, and Honeycomb Energy alone will exceed 2TWh. Looking at the demand side, research shows that by 2025, the demand for power batteries in China and the world will reach 600GWh and 1.2TWh respectively. This means that in 2025, the production capacity of a few leading domestic companies can reach twice the global demand. In recent years, the industry has been saying that high-quality production capacity is insufficient. With this large-scale expansion, there is a high probability that there will be excess high-quality production capacity in the next few years.

So how do leading companies with high-quality production capacity choose a competitive strategy? This is a question that the author has been thinking about recently. After consulting a large number of literatures and in-depth exchanges with customers, partners and scholars in the industry, through many discussions, several strategic options have been summarized for reference in the industry.

When auto parts, can only choose low-cost competitive strategy

In “Competitive Strategy Orientation and Corporate Performance – Based on Data Research of Listed Companies in Automobile Manufacturing Industry”, Wu Jianhua took 38 listed companies in the automobile manufacturing industry as the research object, and the results showed that: (1) 32% of the companies chose low-cost competition strategy , 68% choose the product differentiation competition strategy (2) Up to 90% of the companies’ competitive strategies do not match their performance levels (3) The low-cost strategy is positively correlated with the company’s performance, indicating that the strategic goal is not achieved because the implementation of the low-cost strategy does not meet the standards (4) Differentiation strategy is significantly negatively correlated with corporate performance, indicating that the reason for the low performance level of companies implementing differentiated strategy lies in the inappropriate choice of strategy.

Putting it in plain language means: no matter how tall you are, at the level of auto parts, the low-cost strategy is the most effective, and there are not many differentiated options. Enterprises should further expand their scale, exert the effect of increasing returns at a reasonable scale level, control costs, improve production efficiency, ensure the effective implementation of strategies, and improve their business performance.

Specific to power battery companies, the common ways to reduce procurement costs in the industry mainly include: technology cost reduction, business cost reduction, marketing cost reduction and cost reduction through localized procurement and centralized procurement.

1. Technical cost reduction

The cost reduction of technology is mainly reflected in the product design and production process optimization stage, the use of material systems, positive and negative materials, diaphragms, copper foils, and various auxiliary materials, and the amount of energy obtained under the same amount of use. It includes not only the design optimization of the product itself, but also the optimization of the production process to improve the pass-through rate and the pass rate. Therefore, the design and production process links directly affect the cost structure of the product, which in turn affects the profit of the product. For example, the introduction of dry process can improve performance, increase energy density and save plant area; develop sodium and manganese batteries, which can use common metal elements instead of rare metals to make batteries and so on.

2. Business cost reduction

Most companies attribute the responsibility for cost reduction to the purchasing department, and the purchasing department is mainly responsible for business cost reduction.

The mode of tender procurement has strong flexibility and operability. Through tender procurement, the procurement price can be reduced, better payment methods and longer payment periods can be obtained, and more potential suppliers can be developed. The bidding mode commonly used by large-scale enterprises.

At the same time, it is involved in the construction and investment of the upstream core supply chain, and stabilizes and reduces the procurement cost by locking the supply volume and price. In the final analysis, the price negotiation is a process in which the supply and demand sides compete with each other on the balance of the interests of both parties.

Extending payment terms and adjusting payment methods goes beyond price and is a way to reduce costs through flexible financial strategies. In addition, optimizing transportation methods and reducing transportation costs are also one of the ways to reduce costs. The Ningde era opened up the upstream and downstream to establish its own ecosystem is a case.

3. Marketing cost reduction

Marketing cost reduction means that the cost reduction of products is integrated into the marketing process. In the order-based marketing model, the concept of cost reduction is instilled in each salesperson, guiding customers to choose standardized and unified products, reducing or even avoiding individuality. To meet the needs of the customer, make the products selected by customers consistent with the general products of the enterprise.

Marketing cost reduction is a link that is easily overlooked by most companies. However, under the current situation of order-based production of large customers of power batteries, marketing cost reduction is the source of cost reduction. Locking in mass supply to key customers is the key to reducing marketing costs. LG is bound to Tesla, China Innovation Airlines is bound to GAC, and Honeycomb has the Great Wall.

4. Localized Procurement and Centralized Procurement

Due to the smallest procurement radius, localized procurement can achieve the lowest transportation cost, greatly shorten the procurement cycle, minimize warehouse inventory, and even achieve zero inventory, minimizing inventory costs.

Centralized procurement is also called the centralization of procurement. The method of centralized procurement is suitable for bulk materials. The variety is single, and it can reach a certain quantity and purchase amount. In business negotiations, the buyer has a certain bargaining power, otherwise it will lose the ability of centralized procurement. significance. The advantages of localized procurement and centralized procurement are becoming more and more obvious, and they have become an important procurement method for large-scale enterprises, which can realize an industrialized cluster with a complete supporting system. For example, Changzhou in Jiangsu, Yibin in Sichuan, and Ningde in Fujian have formed a cluster of lithium battery industries.

Get involved in vehicle manufacturing and sales to get a premium

The author has been expounding a fact: throughout the century-old automobile history, Mercedes-Benz, BMW, Audi, Honda, etc. all came from the core component of the car engine to the automobile industry, and none of them came from the carriage company. As the core of the smart electric vehicle, the power battery accounts for more than one-third of the cost of the whole vehicle, which is far higher than the cost of the engine in the oil vehicle. Why can’t there be several vehicle companies?

In this strategic choice, CATL, which ranks first in the world, is already making a layout. CATL is already the second largest shareholder of Avita, a smart electric vehicle technology company. CATL’s smart technology integrated electric chassis and its supporting integrated die-casting project have all started. In addition to smart electric vehicles, two or three-wheeled vehicles and motorcycles are also an option.

On March 29, the first round of financing of Avita Technology was completed, the registered capital increased to 1.172 billion, and CATL held 23.99% of the shares, officially becoming the second largest shareholder of Avita Technology. The absent 5% of Huawei’s shares are held by the Fujian Times Mindong New Energy Industry Equity Investment Partnership, an affiliate of CATL. After the completion of the delivery, the top five shareholders are Changan Automobile 39.2%, CATL 23.99%, Chongqing Chengan 19.01%, Nanfang Assets 8.73%, and Fujian Times Mindong 5%.

According to previously announced information, Avita’s first car is a pure electric coupe mid-size SUV, built on the smart electric networked vehicle platform (CHN) jointly developed by Changan, Huawei and CATL, providing 400TOPs of intelligent driving computing power , and the vehicle will have an endurance level of more than 700km, the acceleration time of 0-100km/h is less than 4 seconds, and the use of 200kW fast charging technology. The car will be officially released in the second quarter of 2022, and the first mass production deliveries will be achieved in the following three quarters. The first body-in-white has been successfully rolled off the production line at the Chongqing plant. In the next five years, Avita will launch four models.

In addition to investing in Avita Technology to become the second largest shareholder, CATL’s investment targets in complete vehicles also include Nezha Auto, Ji Krypton Auto, AIWAYS Auto, BAIC Blue Valley, VALMET Auto, etc. In the integrated electric chassis project that may be popular in the future, the Ningde era is also investing heavily.

On February 19, the groundbreaking ceremony of CATL (Shanghai) Intelligent Technology Integrated Electric Chassis Development Project and Ruiting Times Shanghai Intelligent Power System Project (Phase II) were held in Lingang, Shanghai. In line with the rapid development trend of the new energy vehicle industry, Ningde Times, together with Sanxiang New Materials Co., Ltd., Jiangsu Wanshun Electromechanical Group Co., Ltd., and Guangdong Wenda Magnesium Technology Co., Ltd., jointly invested in “magnesium-aluminum alloy die-casting” in Shouning County, Ningde. project”. The project introduces a batch of die-casting units, including 2500T and 5000T models. A few days ago, the production line of the project has been successfully tested and has the conditions for mass production.

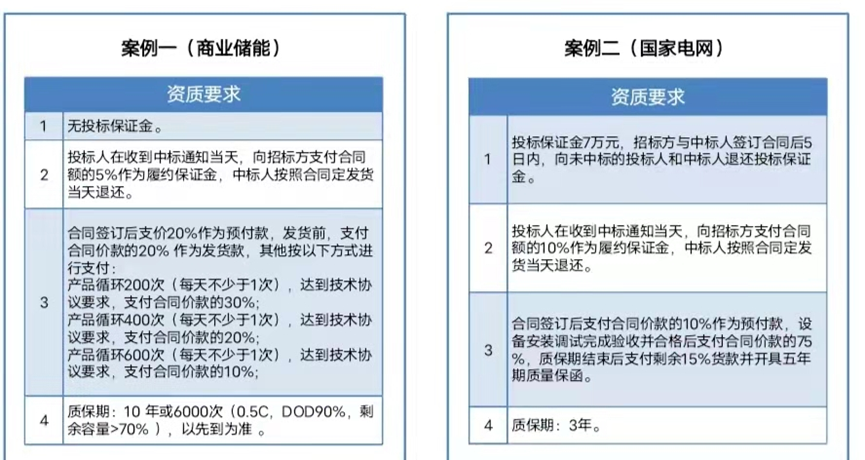

It is better to be an auto parts supplier if you are involved in energy storage on the grid side or power generation side

In 2020, the author was commissioned by an international manufacturer to conduct a detailed domestic electrochemical energy storage research. Due to the expiration of the confidentiality period, the relevant research conclusions are now made public for your reference.

1. Commercial energy storage is essentially a financial product. To calculate the profit model based on 5-year repayment and 5-year operating profit, it must have strong financial operation capabilities.

2. The State Grid project is essentially an engineering project, deducting 15% of the quality deposit, and paying after acceptance. The period from bidding to settlement is 6-12 months, and it also requires high financial capabilities.

3. Most 5G base station projects are tendered by towers, and the period from tendering to settlement is between 3-6 months. At present, most of the companies that are actively deploying energy storage are listed companies, which confirms that energy storage has a high demand for funds.

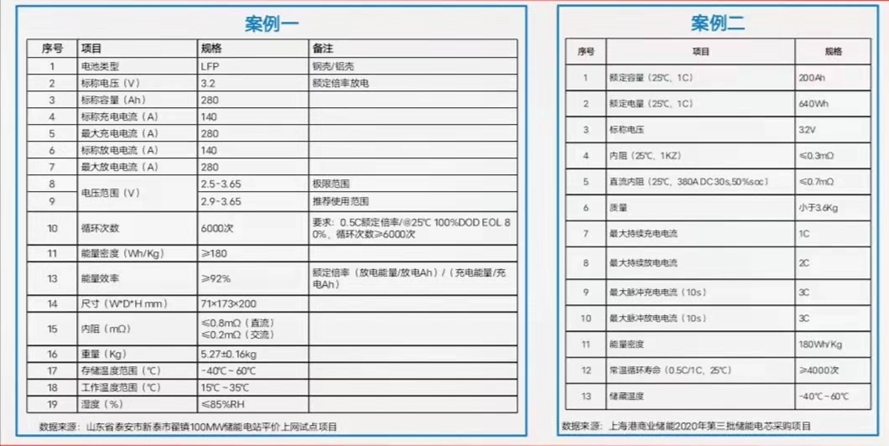

4. All domestic energy storage requires the use of lithium iron phosphate batteries, and new batteries are required except for the base station backup power supply.

5. Battery performance mainly requires cycle times and magnification. Frequency modulation requires power batteries. Peak shaving and energy storage batteries are ordinary energy batteries. The profit is still good in terms of monomer or system price.

6. According to the survey of the TOP10 battery factories, a conclusion is drawn: the manufacturers with lithium iron phosphate production capacity are all laying out energy storage, and most of the factories without lithium iron phosphate production capacity do not deploy energy storage (except for Xinwangda, which outsources Lithium iron phosphate batteries are used for energy storage, which is related to the fact that it started as a PACK factory), which shows that leading companies pay more attention to automotive batteries.

After carefully studying the product requirements and trading conditions of energy storage, it is actually not as good as an auto parts supplier. According to EESA statistics, the installed capacity of domestic electrochemical energy storage projects of Chinese enterprises in 2021 will be 5.85GWh, while the installed capacity of power batteries in China will be 154.5 GWh in the same period. It is called the Ningde era, and it is the first translation of the power battery! The data also supports my judgment two years ago is correct.

Involved in home commercial energy storage operation or power exchange to become an energy operator

On January 18, Ningde Times’ wholly-owned subsidiary, Times Dianfu, released the power exchange service brand EVOGO, and simultaneously announced the so-called “chocolate” combined power exchange overall solution. Many people in the industry think from the perspective of solving mileage anxiety, charging anxiety and expanding market share. I think they are all right, but not all!

In fact, the underlying logic of power exchange, household and commercial energy storage operations is the transformation of battery factories from product manufacturers to new energy operators! Transforming into a new energy operator has four advantages:

First, the market space of operators is larger than that of manufacturers. When a battery is sold as an auto part, the sale ends once. If it is used for energy storage or power exchange, the battery will have electricity fee income in addition to the rent. The rent should cover the cost of the battery in two or three years. The share of the electricity fee income is profit. This market space Roughly more than three times as much as pure sales.

According to the power exchange module of Hangzhou Bertan Technology, each block of electricity is 15 kWh, and if a one-time sale is made, it will be settled at 15,000 yuan; according to the power exchange calculation without rent: 2.50 yuan per kWh of electricity, 300 times a year, and annual electricity bill Settling 11250, according to 5 years, is 56250 revenue, which is 3.75 times the single sales revenue.

Second, the penetration rate of operators has a large room for growth. At present, energy storage and power exchange are still at a relatively low level, the penetration rate is relatively low, and there is still a lot of room for growth in the future.

3. The energy revolution will drive the development of electricity and drive the development of energy storage. In the future, energy consumption will be more realized in the form of electricity. Coupled with the country’s big goal of achieving carbon neutrality, it may be that most of the heating needs to be converted to electric heating. Therefore, the proportion of electricity consumption in energy consumption will increase, and there will be more energy storage for domestic and commercial use.

Fourth, the operating stability of operators will be relatively better. On the other hand, manufacturers in the middle and lower reaches of new energy have been affected by the surge in upstream raw material prices, and the recent pressure is also considerable. This is precisely because the industrial chain of new energy is very long, and changes in profit distribution will occur in different time periods, which leads to higher volatility of profits and greater operational volatility of manufacturing companies.

finally

Historically speaking, power batteries, a technology- and capital-intensive industry, will eventually gradually become an ordinary manufacturing industry and obtain the average profit of ordinary manufacturing. The best companies will also fail to keep up with the trend of the technological industry revolution and gradually become second-class companies, but in the era when they lead the wave, they are undoubtedly the most valuable. Don’t want to be drawn into this trend, and make different strategic choices to cross the cycle. Of course, the introduction of new technologies such as dry process and solid-state batteries is also extending the technological attributes of power battery companies.