(Source: Wugang Futures Microservices)

Wugang Futures Microservices

1. Since its listing, the activity of cast aluminum alloy futures has been weak

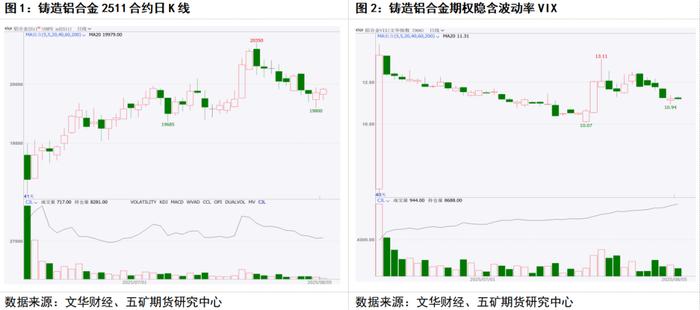

Since its listing on June 10 this year, the main contract prices have increased compared with when they were listed, but the transactions and holdings show that the activity of the variety is relatively weak. As of August 4, the holdings of cast aluminum alloy futures weighted contracts were about 10,000 lots, and the trading volume dropped from 58,000 lots in the early stage of listing to less than 2,000 lots recently. At the same time, the price of cast aluminum alloys fluctuated relatively stable, and the implicit volatility average of options contracts was about 11.

2. Cast aluminum alloy futures activity is weak due to multiple reasons

The author believes that the main reasons for the weak activity of cast aluminum alloy futures after listing are as follows: First, cast aluminum alloys are not priced in the industrial chain, second, the seasonal impact in recent times, and third, the current time is long before the first delivery, and market participants are relatively cautious.

First of all, in terms of pricing power, cast aluminum alloys are located in the middle and lower reaches of the aluminum industry chain, and their prices are affected by multiple factors, including market supply and demand, raw material costs, industry policies, etc. Among them, scrap aluminum is the largest cost of cast aluminum alloys, accounting for about 90%. Therefore, its price has an extremely important impact on the price of cast aluminum alloys. At the same time, in recent years, the domestic cast aluminum alloy production capacity has continued to expand significantly, the production end capacity utilization rate is insufficient (less than 60%), the industry competition is relatively incentive, and the products of the leading manufacturers are highly competitive, but most general-purpose products are relatively homogeneous. Compared with downstream automobile and vehicle industries, cast aluminum alloy concentration is low and there is a lack of pricing voice, resulting in the price of cast aluminum alloys being based on cost pricing, and their prices are highly positively correlated, and the two usually fluctuate within a certain price difference range.

From the actual market operation, the fluctuation rhythm of cast aluminum alloy futures after listing is relatively consistent with aluminum futures. The AD2511 contract basically fluctuates within the range of discounted AL2511 contract 400-600 yuan/ton, and the price of cast aluminum alloy is still priced according to the aluminum price to a large extent.

In addition, although the country recently proposed to comprehensively rectify the “intra-roll” competition, the cast aluminum alloy industry also has a large space for “anti-roll” due to the low operating rate and continuous pressure on production profits. However, due to the low industry concentration, many manufacturers and scattered, it is difficult to reduce large-scale production, resulting in limited response to the “anti-roll” policy.

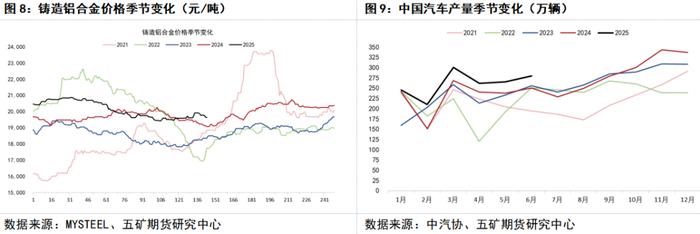

Second, seasonal influence. Cast aluminum alloys are mainly used in industries with low purity requirements and demand for lightweight, corrosion resistance and complex structures. The downstream industries are mainly automobiles, motorcycles, machinery and equipment, household appliances, etc., among which automobiles and motorcycles account for more than 70%, which is the main downstream. The seasonal characteristics of automobile and motorcycle production are relatively obvious. April-June and September-December are the traditional peak production seasons, while the suspension of production during the Spring Festival from January to March and the reduction in orders during the summer high temperature holidays from July to August is the traditional off-season. Most cast aluminum alloy manufacturers determine production based on sales, so during the downstream off-season from July to August, the industry's operating rate is often low seasonally. The changes in the production and sales peak and off-seasons have caused certain seasonal fluctuations in the prices of cast aluminum alloys, and the prices in the peak season are usually stronger and the prices in the off-season are weak.

The current cast aluminum alloy is in the off-season for production and sales. The weak sales make its own price lack support from the demand side, and also makes the price of cast aluminum alloy mainly fluctuate with aluminum futures (i.e., cost side).

Finally, the first delivery contract for cast aluminum alloy is 2511 contract, and there is still a long time before delivery, and the market uncertainty is high. The reason is that the silicon and copper content in the standard delivery products of cast aluminum alloy are both range values, and the content can be delivered as long as it meets the range specified in the delivery products. In this case, there is a concept of the cheapest delivery product for cast aluminum alloy (increase the silicon content to close to the upper limit, reduce the copper and aluminum content to reduce costs). In addition, the 2511 contract is a peak season contract, and its price is a certain premium compared to spot, which reduces the willingness to take over goods and participate in the market. At the same time, the existence of price spreads and the cheapest delivery products is more beneficial to the seller's delivery, and the futures and spot merchants are still active in buying goods. The cast aluminum alloy inventory is transferred from the factory warehouse to the social warehouse, but the cost support and the uncertainty of the peak season contract price have also certainly affected the seller's enthusiasm.

Referring to the situation after the listing of alumina, alumina was officially listed in late June 2023, with the first delivery contract being 2311 contract. At that time, before the 2311 contract was delivered, the transaction of alumina positions was relatively inactive. However, starting from the start of the contract, the market activity gradually increased, and alumina futures were further active in 2024.

3. Future market prospects for cast aluminum alloys

In the medium and short term, the downstream of cast aluminum alloys are gradually transitioning from the off-season to the relative peak season. The impact of the demand side on the pricing of cast aluminum alloys is expected to increase. However, considering that the futures and spot price difference is still large and the industry's capacity utilization rate is low, the futures side still faces considerable market delivery pressure, and its price may still be difficult to escape from the anchor of the cost side. It is expected to continue to maintain a certain price difference fluctuation with the aluminum price. In terms of aluminum prices, domestic electrolytic aluminum operating capacity is close to the upper limit and relatively low inventory continues to support aluminum prices. However, if the US tariff policy is maintained, the pressure on the aluminum demand side will increase, and the center of gravity of aluminum prices may shift down, limiting the rebound height of cast aluminum alloy prices in the peak season.

Over time, adjustments in cast aluminum alloy production capacity output, demand changes and potential carbon premiums may be important influencing factors in price fluctuations. If the “anti-involvement” policy can significantly slow down the growth of industry production capacity, cast aluminum alloys will have stronger independent pricing capabilities and there will be greater room for price difference with aluminum.

Disclaimer: The information in this report is from public information or on-site research. Our company and researchers do not make any guarantees on the accuracy and completeness of the information. The information and opinions in this report reflect the judgments when the report was first published and may be adjusted at any time; the information and opinions in the report do not constitute an investment offer or a sale proposal, and the investment decisions and results made by investors have nothing to do with the company and the author. Investment is risky, so be cautious when entering the market.